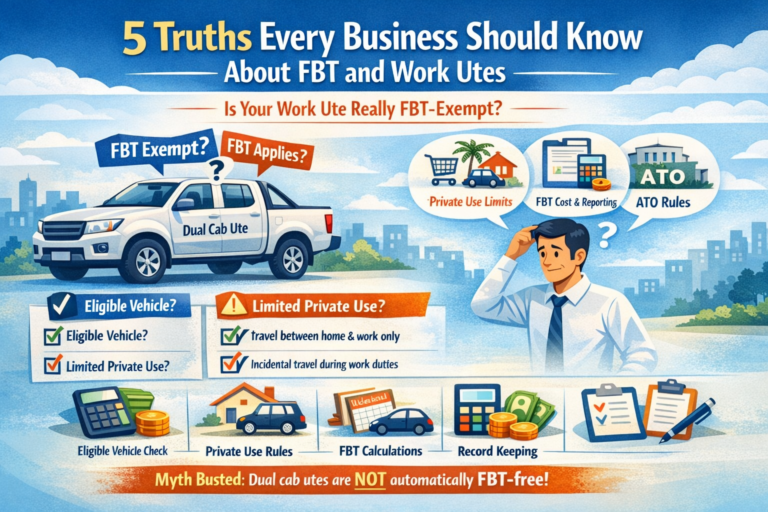

5 Truths Every Business Should Know About FBT and Work Utes

Many businesses believe that providing a dual cab ute to an employee is automatically exempt from fringe benefits tax (FBT). This is a common myth — and relying on it can result in an unexpected FBT liability.

While some work utes can be exempt from FBT, the exemption only applies if strict conditions are met. Both the type of vehicle and the employee’s private use are critical.

This guide explains how FBT applies to work utes, when an exemption is available, and what businesses need to do to stay compliant.

1. What Is Fringe Benefits Tax (FBT)?

Fringe benefits tax (FBT) is a tax employers pay when they provide non‑cash benefits to employees or their associates. One of the most common fringe benefits is the private use of a work vehicle.

FBT:

- Is separate from income tax

- Is paid by the employer, not the employee

- Applies even if private use is allowed incidentally

A work ute is only exempt from FBT if it satisfies both exemption conditions set by the ATO.

2. Condition One: The Vehicle Must Be an Eligible Vehicle

To qualify for an FBT exemption, the ute must meet the ATO’s definition of an eligible vehicle.

A dual cab ute may qualify if it is:

- Designed to carry a load of one tonne or more, or

- Designed to carry more than eight passengers (including the driver), or

- Designed to carry a load of less than one tonne and not primarily designed to carry passengers

Most dual cab utes in Australia satisfy this first condition — but this alone does not guarantee an FBT exemption.

3. Condition Two: Private Use Must Be Limited

This is where many businesses get caught out.

Even if a dual cab ute is an eligible vehicle, private use must be minor, infrequent and irregular under ATO guidance.

What Limited Private Use Looks Like

Examples of acceptable private use include:

- Travel between home and work

- Incidental travel during work duties

- Occasional, one‑off personal trips (such as a trip to the tip)

When FBT Applies

If an employee uses the work ute for:

- Regular school drop‑offs

- Weekend getaways

- Ongoing shopping trips

- General family use

the limited private use condition is not met — and FBT will apply, even if the vehicle is a dual cab ute.

4. What Happens When FBT Applies to a Work Ute?

If private use exceeds the allowed threshold, employers must meet their FBT obligations.

This includes:

- Calculating the taxable value of the fringe benefit

- Working out the FBT payable

- Lodging an FBT return

- Reporting reportable fringe benefits on the employee’s income statement or payment summary

The taxable value depends on how the vehicle is used and may be calculated using:

- The operating cost method, or

- The cents per kilometre method

The correct method will depend on your specific circumstances.

5. Record‑Keeping Still Matters — Even for Exempt Utes

Even if you believe your work ute qualifies for an FBT exemption, record‑keeping is essential.

While a formal logbook is not required for exempt vehicles, employers should be able to demonstrate that private use remains limited.

Good practices include:

- Periodic odometer checks

- Comparing kilometres travelled against expected work usage

- Having clear internal policies on vehicle use

Without evidence, an FBT exemption may be difficult to support if reviewed.

Source: Ato.gov.au

Key Takeaways for Businesses

- Dual cab utes are not automatically FBT‑exempt

- Both vehicle eligibility and limited private use must be satisfied

- Regular personal use triggers FBT

- Employers are responsible for calculating, reporting, and paying FBT

- Good records reduce compliance risk