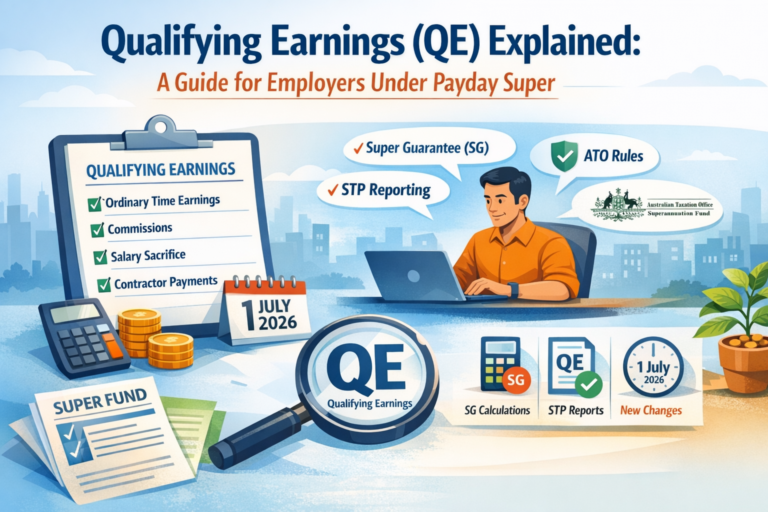

Qualifying Earnings (QE): What It Means for Employers Under Payday Super

Qualifying earnings (QE) are a new superannuation concept introduced by the Australian Taxation Office (ATO) as part of the Payday Super reforms starting 1 July 2026.

From this date, employers must use qualifying earnings as the standard earnings base for calculating and reporting Super Guarantee (SG). This article explains what qualifying earnings are, how they affect employers, and how to prepare for QE reporting under Payday Super. Please see our article Payday Super 2026: A Quick Guide for Employers for more details on the Payday Super 2026 changes.

What Are Qualifying Earnings (QE)?

Qualifying earnings (QE) define which payments employers must use to calculate Super Guarantee (SG) contributions under Payday Super.

The ATO introduced QE to create a single, consistent earnings base for both super payments and reporting.

Payments Included in Qualifying Earnings

Qualifying earnings include:

- Ordinary time earnings (OTE)

- All commissions paid to an employee

- Salary sacrifice amounts that would have qualified as QE if they had not been sacrificed to super

- Earnings paid to workers under the expanded definition of employee, including some independent contractors paid mainly for their labour

This expanded definition ensures more workers receive superannuation protections under Payday Super.

What Do Qualifying Earnings Mean for Employers?

From 1 July 2026, all employers must calculate both:

- Super Guarantee (SG), and

- Super Guarantee Charge (SGC)

using qualifying earnings.

What’s Changed?

Previously, employers used:

- Ordinary time earnings (OTE) to calculate SG, and

- A different earnings base to calculate SGC if super was paid late.

Under Payday Super, QE replaces both, simplifying compliance and reporting.

✅ For most employers, this change does not increase the amount of super paid — it standardises how and when super is calculated and reported.

Who Is Eligible for Super Guarantee Under QE?

Most employees are entitled to Super Guarantee contributions. However, under the expanded QE rules, some workers who were previously excluded may now qualify.

Employees and Contractors

Employers may need to pay super for:

- Employees under standard employment arrangements

- Independent contractors paid mainly for their labour, who are treated as employees for superannuation purposes

If you’re unsure whether a worker qualifies, the ATO provides a Superannuation Guarantee eligibility decision tool to help determine SG obligations, including for contractors.

How Qualifying Earnings Are Reported in Single Touch Payroll (STP)

From 1 July 2026, employers must report additional information through Single Touch Payroll (STP).

Mandatory STP Reporting Requirements

Employers must report:

- Each employee’s year‑to‑date qualifying earnings (QE), and

- Each employee’s year‑to‑date super liability

Reporting for Independent Contractors

Reporting payments made to independent contractors paid mainly for their labour is optional.

However, if employers choose to report these workers through STP, they must report both:

- Qualifying earnings, and

- Super liability

Partial reporting is not permitted.

Key STP Reporting Milestones Employers Need to Know

- From 1 July 2026

Reporting qualifying earnings and super liability through STP becomes mandatory - From 1 July 2027

STP reports that do not include QE or super liability will be rejected by the ATO

Source: ato.gov.au

These milestones make early preparation critical.

Why Employers Must Report Both QE and Super Liability

Under Payday Super, qualifying earnings replace ordinary time earnings as the base for calculating Super Guarantee.

However, some employers may have additional super obligations under:

- Awards

- Enterprise agreements

- Employment contracts

These extra contributions may fall outside qualifying earnings, but employers can still report them as super liability through STP.

Reporting both figures ensures:

- Accurate compliance tracking

- Clear distinction between SG obligations and additional super payments

- Alignment with ATO reporting requirements

How Employers Can Prepare for Qualifying Earnings Reporting

To prepare for QE reporting under Payday Super, employers should act early.

Practical Preparation Steps

- Confirm with your payroll or digital service provider when their software will support QE reporting

- Review payroll and STP processes to ensure:

- Pay codes are mapped correctly to qualifying earnings

- Employee details are accurate and up to date

- STP lodgements are made on time and without errors

For official guidance, updates, and resources, visit:

👉 ato.gov.au/paydaysuper

Key Takeaways for Employers

- Qualifying earnings (QE) are the new standard earnings base for super

- QE applies to both Super Guarantee and Super Guarantee Charge

- QE reporting through STP becomes mandatory from 1 July 2026

- From 1 July 2027, incomplete STP reports will be rejected

- Early payroll preparation reduces compliance risk