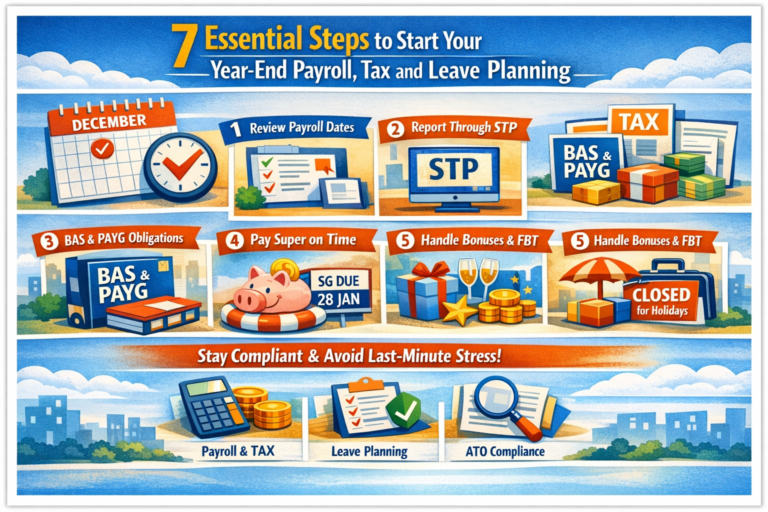

7 Essential Steps to Start Your Year‑End Payroll, Tax and Leave Planning

The year‑end holiday period can put real pressure on businesses. Whether you expect a seasonal surge or plan a temporary shutdown, early planning for payroll, tax, superannuation and employee leave is critical.

Starting your year‑end planning now helps you:

- Stay compliant with ATO and workplace obligations

- Manage cash flow with confidence

- Avoid last‑minute errors, penalties, and employee disputes

1. Review Your Year‑End Payroll Calendar Early

Begin by reviewing your payroll schedule to identify:

- Paydays that fall on public holidays or weekends

- Pay runs affected by a business shutdown

- Bank cut‑off times during the holiday period

If a scheduled payday falls on a public holiday, bring the pay run forward so employees receive their wages on time.

If pay dates change temporarily, notify employees in writing. While the ATO may allow lodgment and payment on the next business day when due dates fall on a public holiday, this concession does not apply to paying wages late.

2. Report Every Pay Run Through STP on Time

All pay runs — including early or adjusted payments — must be reported through Single Touch Payroll (STP) on or before payday.

This includes:

- Wages paid before a shutdown

- Bonuses processed at year‑end

- Leave payments made in advance

Accurate and timely STP reporting helps ensure employee income statements remain correct and reduces follow‑up issues in the new year.

3. Stay on Track With PAYG Withholding and BAS Obligations

Holiday periods don’t pause your tax obligations.

Make sure:

- PAYG withholding is reported and paid on time

- BAS lodgments remain up to date

If you anticipate difficulty meeting due dates, speak with your tax adviser and contact the ATO early. Proactive communication can help prevent penalties and interest from applying.

4. Pay Super Guarantee Contributions on Time

Super Guarantee (SG) is often overlooked during the holiday rush.

Remember:

- SG applies to wages and paid leave, including annual leave and public holiday pay

- October–December quarter super must be received by employees’ super funds by 28 January

Pay early to allow for bank processing delays and to avoid:

- Super Guarantee Charge (SGC)

- Interest and penalties

- Loss of tax deductibility

5. Handle Bonuses, Gifts and FBT Correctly

If you pay year‑end bonuses, process them through payroll and withhold the correct amount of tax.

Also review:

- Staff gifts

- End‑of‑year functions

- Non‑cash benefits

Some items may qualify for the minor benefits exemption, but this depends on value, frequency and circumstances. Keep accurate records to support your FBT position.

6. Apply Public Holiday and Leave Entitlements Properly

When a public holiday falls on a day an employee would normally work and they don’t attend work:

- Pay full‑time and part‑time employees their base rate for ordinary hours

You may request employees to work on a public holiday, but:

- The request must be reasonable

- Employees may refuse on reasonable grounds

If employees do work, apply the correct:

- Penalty rates, or

- Time off in lieu (TOIL), where permitted

If a public holiday occurs during annual leave, treat the day as a public holiday, not a leave day.

7. Prepare Carefully for Holiday Shutdowns

You can only direct employees to take annual leave during a shutdown if:

- An applicable award or registered agreement allows it, and

- Required notice is given in writing

If employees don’t have enough accrued leave:

- Many awards allow leave in advance, or

- Unpaid leave by agreement

Always document these arrangements in writing and confirm whether leave loading applies to annual leave taken during the shutdown. Ensure your payroll system calculates leave loading correctly.

Key Takeaways for Employers

- Start year‑end payroll and leave planning early

- Adjust pay runs around public holidays and shutdowns

- Keep STP, PAYG, BAS and super obligations on track

- Apply awards, agreements and FBT rules correctly

- Clear planning reduces compliance risk and stress

ATO References

For official guidance on employer payroll, tax, superannuation and year‑end obligations, refer to the following Australian Taxation Office resources:

Important Disclaimer

This material contains general information only and does not constitute advice. Workplace laws and tax obligations can change, and outcomes depend on individual circumstances. We recommend seeking formal advice before acting.